Life insurance coverage is a contract between an insurer and a policyholder. A life insurance coverage policy guarantees the insurance company pays an amount of cash to called recipients when the insured policyholder dies, in exchange for the premiums paid by the policyholder throughout their lifetime. Life insurance is a legally binding contract.

For a life insurance policy to remain in force, the insurance policy holder needs to pay a single premium up front or pay regular premiums in time. When the insured passes away, the policy's called recipients will get the policy's stated value, or survivor benefit. Term life insurance policies end after a specific number of years.

A life insurance coverage policy is just as good as the monetary strength of the business that issues it. State guaranty funds might pay claims if the company can't. Ready to buy life insurance coverage? Read our reviews of the best life insurance business: Life insurance coverage provides financial backing to making it through dependents or other beneficiaries after the death of an insured.

Life Insurance Diagram Quizletquizlet.com

Life Insurance Diagram Quizletquizlet.com

Life insurance can make certain the kids will have the funds they need until they can support themselves. For kids who require lifelong care and will never be self-dependent, life insurance coverage can make certain their requirements will be fulfilled after their moms and dads pass away. The survivor benefit can be utilized to fund a special requirements trust that a fiduciary will manage for the adult child's benefit.

An example would be an engaged couple who took out a joint mortgage to purchase their very first home. Lots of adult children sacrifice by taking time off work to take care of an elderly moms and dad who requires aid. This aid might likewise include direct financial assistance. Life insurance can assist repay the adult child's expenses when the moms and dad passes away.

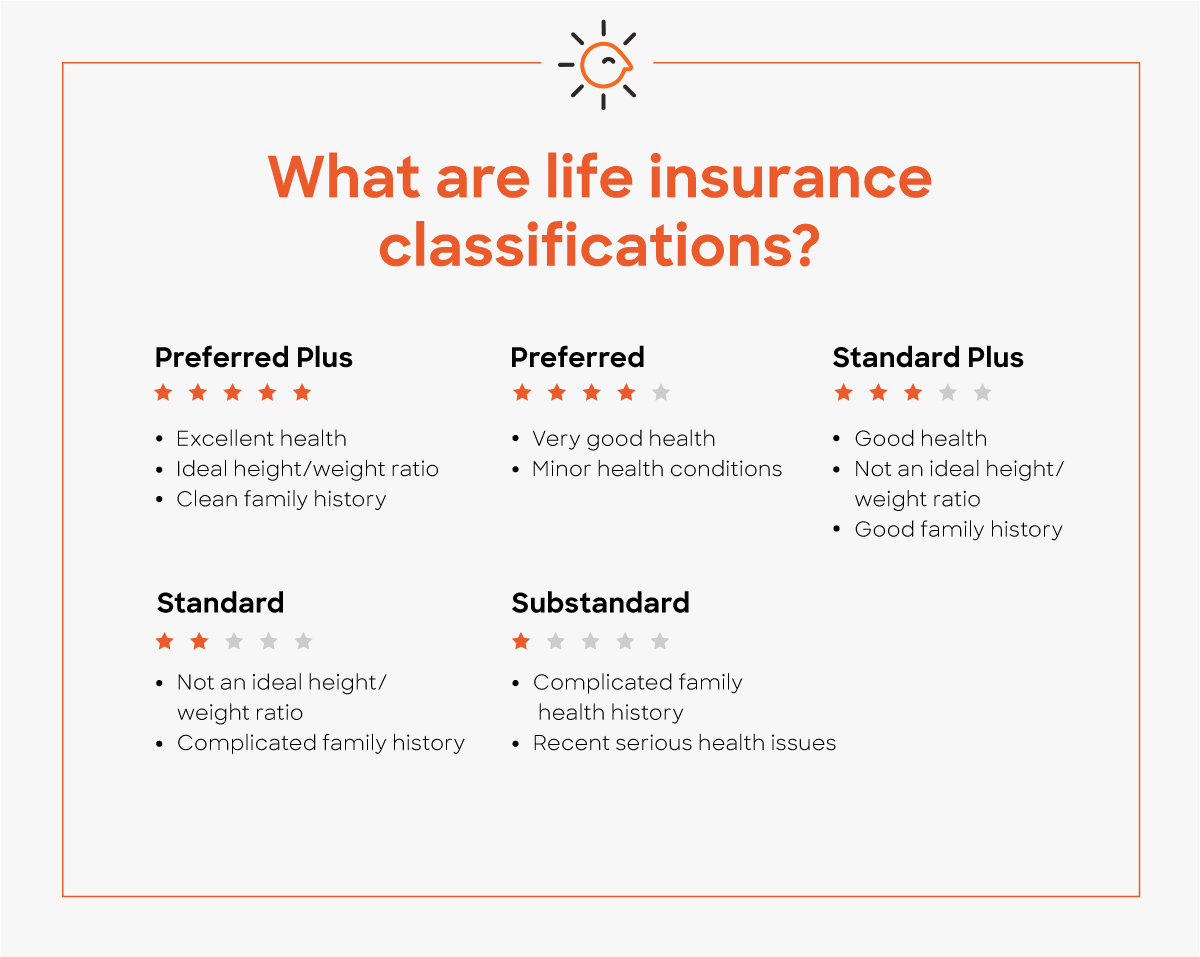

The more youthful and healthier you are, the lower your insurance coverage premiums. A 20-something grownup may purchase a policy even without having dependents if there is an expectation to have them in the future. Life insurance can offer funds to cover the taxes and keep the amount of the estate intact.' A little life insurance coverage policy can provide funds to honor a liked one's passing.

Term Life Insurance Kenya - Compare ...calculator8.com

Term Life Insurance Kenya - Compare ...calculator8.com

Rather of selecting in between a pension payment that provides a spousal advantage and one that does not, pensioners can select to accept their full pension and utilize a few of the money to buy life insurance to benefit their spouse. This strategy is called pension maximization. A life insurance coverage policy can has 2 primary componentsa survivor benefit and a premium.

The death benefit or face value is the quantity of money the insurance provider guarantees to the recipients determined in the policy when the insured passes away. The guaranteed might be a parent, and the recipients may be their children, for example. The guaranteed will pick the desired survivor benefit amount based on the recipients' estimated future requirements.

Premiums are the cash the policyholder spends for insurance coverage. The insurer needs to pay the death advantage when the insured passes away if the policyholder pays the premiums as required, and premiums are determined in part by how likely it is that the insurer will have to pay the policy's survivor benefit based on the insured's life span.

Part of the premium also goes toward the insurance provider's operating costs. Premiums are higher on policies with bigger survivor benefit, people who are higher threat, and permanent policies that build up cash value. The money worth of permanent life insurance serves 2 purposes. It is a cost savings account that the policyholder can utilize throughout the life of the guaranteed; the cash collects on a tax-deferred basis.